Resilient: A single word to capture the U.S. economy over the past five years. It’s remained on solid footing despite an unprecedented upheaval and equally dramatic recovery. But during this period of sometimes-puzzling economic strength, the people haven’t entirely been feeling it: Despite strong numbers on average, consumer sentiment is lackluster.

Economics is a complex, pervasive topic. When you begin to study it, you realize just how much you have to learn. I know that was the case for me, even before graduate school. So, for the general public, misinformation or misunderstandings could certainly prompt part of the gap between sentiment and reality. The easy answer is to assume ignorance. By implying the data is right and the people are wrong, you make it OK for economists, policymakers and journalists to cast aside these “flawed” perspectives.

Whether sentiment is shaping household and broader economic strength or being used by economists to predict spending and saving, how people perceive their economy matters.

This report examines the disconnect between economic data and sentiment, and potential reasons for it. It then discusses why we shouldn’t be too quick to discount how people feel about their economic prospects.

What’s inside

-

How the 50/30/20 budget calculator works

-

What is a simple definition of credit?

-

What is a home equity line of credit?

-

What is the windfall elimination provision?

-

What is the Social Security 2024 COLA increase?

-

Learn more about the good credit range

-

What is personal finance?

-

What is a required minimum distribution (RMD)?

-

What is child identity theft?

-

What is a FICO score and why is it important?

-

What is Do Your Own Will?

-

What is a power of attorney?

-

Can you collect Social Security and a pension at the same time?

-

Biden steps out of the election, endorses Kamala Harris

-

Harris and Trump to debate on Sept. 10

-

Who is leading in the polls?

-

Wharton analysis: Trump’s plans would add $4.1 trillion to deficit

-

Harris proposes an ‘opportunity economy’

-

Who is leading in the polls?

-

What the 15/3 credit hack claims

-

Why the 15/3 credit hack is wrong

-

Credit utilization ratio details

-

What really helps your credit score

-

Explore 28 ways to save money

-

Calculate how much to save each month

-

Estate planning checklist

-

What is a first-time home buyer grant?

-

Why put a house in trust?

-

What are the most important things to put in a will?

-

Conservatorship vs. guardianship

-

When is the best time of year to buy appliances?

-

Collecting a Social Security retirement benefit while working? You could be penalized.

-

7 budgeting tips for everyone

-

How much should you spend on rent?

-

What are refinance closing costs?

-

Who qualifies for spousal retirement benefits after divorce?

-

HELOC and home equity loan interest deduction rules

-

What is debt-to-income ratio?

-

How much does a Disney+ subscription cost per month?

-

Option 1: Use your tablet as a phone over Wi-Fi

-

Why would my credit score drop after paying off debt?

-

Microsoft Office Excel budget templates

-

WSHFC highlights and eligibility requirements

-

How much should you tip a pizza delivery driver?

-

What is full retirement age for Social Security?

-

Good credit utilization follows the 30% rule

-

4 ways to make money blogging

-

Buy: Christmas decorations

-

What is a reverse mortgage?

-

Seek legal advice — but act quickly

-

Work from home jobs often pay more

-

How to make money as a kid

-

Georgia Dream program highlights and eligibility requirements

-

What is a good used iPhone model?

-

What are three kinds of data breaches?

-

How much does HBO Max cost per month?

-

Best time to buy furniture

-

National first-time home buyer programs

-

What is a high net worth individual?

-

How much does an Equinox gym membership cost?

-

What you need to change your name on your Social Security card

-

What is a mortgage recast?

-

1. Choose the smaller model

-

What does it mean to pay yourself first?

-

Tenancy in severalty and estate planning

-

What does it mean to have a thin credit file?

-

Cómo obtener información gratuita de su informe de crédito

-

How letters of administration work

-

What is a hot market in real estate?

-

Apple Music subscription cost

-

What happens when you get sued for debt

-

How to get paid on TikTok

-

Debt avalanche vs. debt snowball

-

Tax benefits of buying a home

-

What does it mean to be ‘in escrow’?

-

Revocable vs. irrevocable trusts: Key differences

-

How to calculate debt-to-income ratio

-

Does a partial payment affect your credit score?

-

How to get your free credit report information

-

At what age is Social Security no longer taxed?

-

SONYMA highlights and eligibility requirements

-

How much are Social Security benefits for nonworking spouses?

-

Buy: Swimwear and lingerie

-

1. Which type of mortgage is best for me?

-

What happened to egg prices in July?

-

What are home equity loans and HELOCs?

-

How much is YouTube TV a month?

-

What is a budget calendar?

-

How a lady bird deed works

-

How voluntary repossession works

-

1. Make sure you’re ready

-

MSHDA highlights and eligibility requirements

-

Why is personal finance important?

-

Is Upwork a legit way to make money?

-

What is a Social Security overpayment?

-

What’s the difference between an attorney and attorney-in-fact?

-

Why retirement age matters

-

Who a balloon mortgage is for

-

How much does it cost to file for bankruptcy?

-

1. Shop at stores with rewards programs

-

Examples of time limits to file for probate in specific states

-

Fixed rates vs. variable rates

-

What a mortgage servicer does

-

What is a cash-out refinance?

-

Make money selling on Amazon

-

What is a cash offer on a house?

-

1. Not knowing how much house you can afford

-

What is a goodwill letter or late payment removal letter?

-

What kinds of coupons does Etsy have?

-

Food and drink

-

NCHFA highlights and eligibility requirements

-

What are Social Security spousal benefits?

-

What does a credit freeze do?

-

1. Buy your own cable modem and router for cheaper Wi-Fi (over time)

-

Irrevocable trusts vs. revocable trusts

-

How to lock your Social Security number for free

-

Should you use home equity or try an alternative way to pay off debt?

-

What is a VA disability rating?

-

The definition of a recession

-

What are the requirements to get a POA in Virginia?

-

Online marketplace and auction sites

-

Does an unused credit card affect your credit score?

-

National first-time home buyer programs

-

How to get paid on YouTube

-

How much is Amazon Prime in 2024?

-

What is a loan modification?

-

When is a payment marked late on credit reports?

-

1. ‘Stack’ store and manufacturer’s coupons

-

Summer driving season kicks off

-

The relationship between debt and inflation

-

What is Amazon Prime Reading?

-

1. Compare sites and deals

-

Pivot to a positive mindset

-

What the president can do about gas prices

-

1. Cut back on premium channels

-

How to pass a rental credit check

-

How much does a wedding cost?

-

Exchange gift cards for ones you actually want

-

How much does a gym membership cost?

-

Allow up to 50% of your income for needs

-

Red flags of debt collection scams

-

What are short-term financial goals?

-

How much does a Gold’s Gym membership cost?

-

Things to do before you go

-

What is the Honey Chrome extension?

-

Reason No. 1: Changes to the formula

-

What is Amazon Music Prime?

-

Important questions to ask a recruiter

-

Is the U.S. economy growing?

-

What is broadband internet?

-

Go with a prepaid plan or carrier

-

Will my debt ever get so old that I won’t have to pay it?

-

Inflation will impact deals

-

How much does a Crunch Fitness membership cost?

-

1. Figure out what living debt-free means to you

-

Why are debt validation and debt verification letters important?

-

Can you refinance a home equity loan?

-

PHFA highlights and eligibility

-

1. Account for all possessions

-

What is VantageScore 4.0?

-

Explore free options first

-

Credit bureau customer service phone numbers

-

How to replace your Social Security card online

-

What are variable expenses?

-

1. Ask the seller to reduce the mortgage rate

-

How much does a 24 Hour Fitness membership cost?

-

Seven steps to basic estate planning

-

Is it realistic to grow your score by 100 points?

-

What is the typical down payment on a house?

-

A mortgage adds to your credit history

-

How much you can earn while on Social Security

-

Why is having a low credit utilization important?

-

What is a cash-out refinance?

-

What a 695 credit score can get you

-

What is a mortgage underwriter?

-

CalHFA highlights and eligibility requirements

-

Figure out your debt load

-

What rights do you have when your car is being repossessed?

-

How do Social Security benefits for children work?

-

How does a HomeStyle renovation loan work?

-

Do vet more than one home inspector

-

Building a Twitch audience

-

What to know before you refinance

-

What is a virtual assistant?

-

How much does Amazon Flex pay?

-

Step 1: Take inventory of your skills

-

What are financial goals?

-

How to get a home equity loan with bad credit

-

1. Get help with utility bills and groceries

-

Know what you’re getting

-

National first-time home buyer programs

-

Reserve tickets with your library card

-

Services available at credit counseling agencies

-

When to apply for Social Security

-

What is a home inspection?

-

Recognize the limits of what you see online

-

Generally, closing a bank account doesn’t affect your credit

-

Best places to sell clothes online

-

How people use reverse mortgages

-

What matters most for VantageScores

-

Do you have to tip an Uber driver?

-

The best places to buy a used iPhone or other cell phone

-

1. Check what you already have and make a list

-

How does revolving credit work?

-

How car loans affect credit

-

3 steps for dealing with a debt collector

-

You should feel good about buying a house if …

-

What is the Homeowner Assistance Fund?

-

Indoor furniture: Winter, summer

-

1. Explore alternative locations

-

How does a transfer on death deed work?

-

1. Review your 401(k)’s payout policy

-

You may be eligible for unemployment benefits

-

Buy: Personal care items you can put on autopilot

-

Get preapproved for a mortgage

-

What is mortgage forbearance?

-

Roof replacement cost breakdown

-

Calculate your wedding budget

-

Buy: TVs and big-ticket tech

-

Do rent payments affect credit?

-

What is a bad credit score?

-

How to make your budget resilient

-

Who’s Taylor Swift anyway?

-

How does a power of attorney work?

-

1. Home equity line of credit (HELOC)

-

4 budgeting methods to consider

-

Costs of caskets versus coffins

-

Pros and cons of a quitclaim deed

-

What are a trustee’s duties?

-

When to leave an unequal inheritance

-

How much does a Planet Fitness membership cost?

-

Work accommodations for bipolar

-

Buy if you can roll with the punches

-

What job makes the most money?

-

How much is the average electric bill?

-

To start, verify your mortgage type

-

Which documents should I save? And for how long?

-

How does a second mortgage work?

-

Brace for another year of high interest rates — and prices

-

What does a real estate lawyer do?

-

What would an opportunity economy look like?

-

Tax breaks now could cause tax pain later

-

Debt levels are hitting new highs

-

Financial confidence grows with age and wealth

-

What you should keep safe

-

Cost-of-living adjustments

-

How much is Sling Freestream per month?

-

SSDI payment schedule for 2024

-

Cell phone statute of limitations

-

Why ADUs are increasingly popular

-

What is the MyFICO credit score?

-

The government almost ran out of money this year

-

Financial stress takes a toll

-

Why life expectancy matters

-

When are you considered a first-time home buyer?

-

Credit scores carry weight

-

How long does it take to build a good credit score?

-

Will paying off credit cards help my credit score?

-

What to say in a thank-you email after an interview

-

Refinance to a lower rate

-

Why is diesel more expensive than gas?

-

5 best gas apps to help you save money

-

1. It’s an upgrade to NerdWallet’s free level

-

Why you’re getting two SSI payments

-

What is zero-based budgeting?

-

Government home loans for buying

-

What’s my full retirement age and how does it affect my benefit at age 63?

-

How to find your Social Security number

-

What information is on a utility bill?

-

Will inflation impact Prime Day deals?

-

How does a financial power of attorney work?

-

Topics that may come up in an interview

-

Do you qualify for Chapter 7 bankruptcy?

-

What is a first-time home buyer class?

-

Tell me more: What is the 50/30/20 rule?

-

Budget money to become a saver

-

Too much debt or too little income

-

With a 650 score, you may pay higher rates than others

-

Do other countries have credit scores?

-

How the windfall elimination provision (WEP) works

-

What will the Social Security COLA increase be in 2025?

-

1. Find a payment strategy or two

-

Know how much data you use

-

How to decide if you need a will, a trust or both

-

What are the three credit bureaus?

-

How to find and evaluate inquiries

-

Retirees’ trillion-dollar allowance

-

1. Check all three credit reports for errors

-

What is a home equity loan?

-

What is a manufactured home?

-

1. Check your account statements

-

How to get a death certificate

-

How to get your finances ready for divorce

-

How the FICO Score 9 is different

-

Average monthly expenses by household size

-

Net income vs. gross income

-

Option 2: Use your tablet like a phone with a data-only plan

-

What is the difference between a garage sale and an estate sale?

-

Types of personal finance software and apps

-

Work accommodations for long COVID

-

How to find your full retirement age

-

What is the average credit score by age?

-

Do medical bills affect your credit?

-

How to build a financial safety net

-

What is a monthly budget?

-

Have you even heard from your advisor?

-

What are the stages of foreclosure?

-

How to create a revocable living trust

-

Late winter and early spring

-

1. Go to the correct site

-

How to improve your financial health

-

How many credit cards is too many or too few?

-

Types of wage garnishment and how it happens

-

Pros of reverse mortgages

-

1. Make sure your financing and cash are all set

-

Build wealth by investing

-

Pros of a condo vs. a house

-

Best cash-back apps of 2024

-

How much earnest money to offer

-

How pay yourself first budgeting works

-

International roaming plans: postpaid

-

Go back-to-school shopping for dinner

-

Pros and cons of a charitable remainder trust

-

Only send money to people you know

-

Cómo leer un informe de crédito y qué buscar

-

Steps to rebuilding credit after bankruptcy

-

Why are buyers willing to waive?

-

Pros and cons of a holographic will

-

How to start selling on Poshmark

-

What should I look for on my Equifax credit report?

-

How much of my Social Security Disability Insurance (SSDI) income is taxable?

-

5 ways to make money from your phone

-

1. Get clear on what you want

-

What about packages and bundles?

-

How ‘pay for delete’ works

-

What is a revocable trust?

-

How to find bankruptcy attorneys to contact

-

Site-built, detached single-family houses

-

What to do before making a partial payment

-

How much does a hard inquiry affect your credit?

-

How does a special needs trust work?

-

You may have a tough time getting a loan or card

-

How much should you save each month?

-

A huge and growing need for help

-

When does checking my credit score lower it?

-

Affordability down across large metros in second quarter

-

2. How much down payment will I need?

-

Triple-check the recipient

-

Why you might want to consider an immediate annuity

-

What is an assumable mortgage?

-

What is a cash-out refinance?

-

Find first-time home buyer programs in your state

-

Fixer-upper mortgage options

-

What day is my September 2024 payment coming?

-

The online life doesn’t leave a paper trail

-

1. Use online valuation tools

-

How to make a will without a lawyer

-

Conservatorship vs. adoption

-

1. Participate in paid market research

-

You can take steps to protect your identity yourself

-

How does home equity work?

-

There’s no shame in having money shame

-

How to freeze your credit with all 3 bureaus

-

Mint vs. NerdWallet at a glance

-

What are the duties of an executor?

-

How your servicer can help if you’re behind on payments

-

How much is YouTube Premium?

-

What a 720 credit score can get you

-

Netflix subscription cost

-

How to start with Amazon Flex

-

Appraisal bias reports are on the rise

-

Examples of financial goals

-

Know the credit score you’ll need

-

Do goodwill letters work?

-

Where to find free identity theft protection

-

Start with an authentic budget

-

How does Experian Boost work?

-

Your credit score could drop if your bank account isn’t in good standing

-

Conservatorship vs. guardianship

-

Does fibromyalgia qualify as a disability for SSDI?

-

How to use the debt snowball method

-

What IdentityForce does and what it costs

-

2. Limit your shopping trips

-

What to do if your data has been compromised in a breach

-

How to check if your credit is frozen

-

What does a kitchen remodel cost?

-

What is the CHOICERenovation loan?

-

How does loan modification work?

-

Does my state have transfer on death deeds?

-

What are the weekly jobless claims?

-

How do I know there’s a late payment on my credit report?

-

What are game apps that pay real money?

-

How to make your savings last longer

-

How much of my credit card should I use?

-

What is ‘cash stuffing’?

-

What minimum credit score is needed to buy a car?

-

2. Be relentless about comparing prices

-

Pros and cons of mausoleums

-

How to get power of attorney

-

Pros and cons of tenancy in severalty

-

2. Use a free TV streaming site or app

-

Why do employers check credit?

-

Who is most likely to have a thin credit file?

-

What to know about Social Security retirement benefits

-

What’s the average credit score?

-

How does a mortgage work?

-

Requirements for a HELOC on an investment property

-

Breakdown of central air costs

-

Potential benefits of filing for bankruptcy

-

What are the features of Amazon Music Prime?

-

Denial rates steady across age groups and states

-

An emergency fund is a top priority for nearly half of Americans

-

How to use a HELOC in retirement

-

1. “Your Social Security number is suspended.”

-

Estimating the costs and how to minimize them

-

This is (sort of) what the Fed wanted to happen

-

1. Search for independent reviews, complaints

-

What does it mean if you have a tax lien?

-

Gas prices by the numbers

-

How to read a credit report and what to look for

-

What must a debt validation letter include?

-

What the lawsuits are about

-

Mortgage rates should trend a little lower

-

1. Competitive offers close deals

-

Opt for gender-neutral products

-

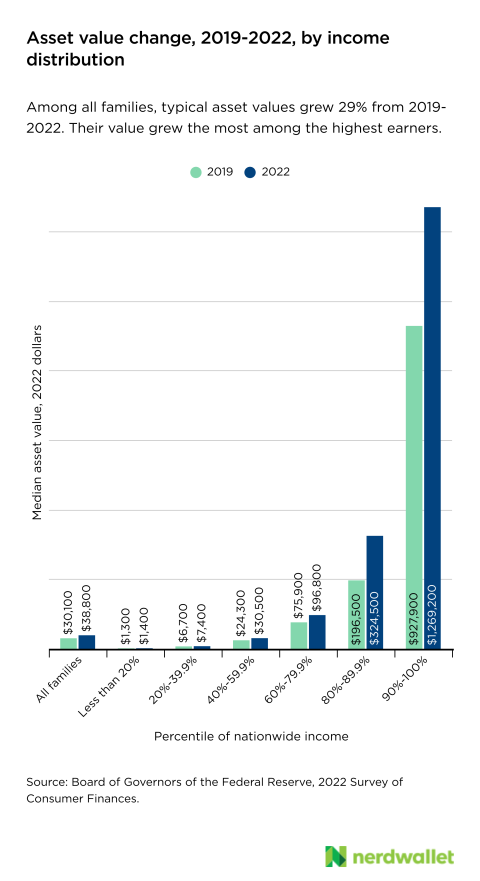

Post-Covid: The economy came back strong, sentiment stayed weak

-

Determine how your Social Security is taxed

-

How much will my Social Security be reduced if I have a pension?

-

Full retirement age for Social Security

-

Who is a credit ghost and who is ‘unscored’?

-

How long does it take to get a replacement Social Security card?

-

Variable expenses examples

-

Understand the financial and legal picture

-

1. Do your homework and gather evidence

-

Latino communities are some of the most at risk when it comes to predatory lending. How can they break cycles?

-

A positive attitude can lead to learning and earning

-

How to work with TaskRabbit

-

TransUnion credit freeze online

-

What’s the purpose of a budget?

-

How to lower your credit utilization

-

How long does underwriting take?

-

Does closing a credit card hurt your credit?

-

How does a home equity loan work?

-

Examples of personal finance in everyday life

-

How does a home warranty work?

-

When should you seek debt relief?

-

Isolation doesn’t guarantee fewer risks — just fewer people

-

Work out how much of your income should go to rent with the 50/30/20 rule

-

Understanding attorneys-in-fact

-

How much Social Security does a divorced spouse get?

-

2. Install a browser extension

-

Overview: Best loans for first-time home buyers

-

What does a virtual assistant do?

-

What’s the difference between a HELOC and a home equity loan?

-

Front-end and back-end DTI

-

Step 2: Focus on monetizable skills and ideas

-

1. Plan for long-term care expenses

-

To compete with cash offers, find out what sellers want

-

How to stop spending money

-

How’s the housing market right now?

-

2. Find money for child care

-

Trusted contacts can’t make changes

-

How to place an Equifax credit freeze

-

Google Sheets budget templates

-

Take advantage of bank or credit union benefits

-

How irrevocable trusts work

-

When should you tip a pizza delivery worker extra?

-

How do Social Security disability benefits work?

-

How to buy a house with cash

-

Full retirement age for Social Security

-

1. Take inventory of your finances

-

What assets should you not put in a living trust?

-

What is a VA disability rating based on?

-

Working from home jobs are growing

-

Ways to earn money as a younger kid

-

What are the different types of POA in Virginia?

-

Give yourself the flexibility to roam

-

The origins of money shame

-

Stores with some of the best return policies

-

Will mortgage forbearance affect my credit?

-

When does a mortgage recast make sense?

-

2. Find a coupon database or a browser extension

-

Expect prices to look like last year

-

2. Buy last year’s model

-

Benefits of an energy-efficient home

-

The hype machine fueled Barbie’s success

-

Types of charitable remainder trusts

-

How to create a quitclaim deed

-

Is filing for bankruptcy right for you?

-

How to create a holographic will

-

Why is this such a seller’s market?

-

What is an example of the debt avalanche strategy?

-

How important a factor is credit mix for your scores?

-

Notable loss of affordability for first-time buyers

-

Definitions: Modular vs. manufactured homes

-

What is the purpose of an appraisal?

-

2. Know how much debt you have

-

Should I carry a balance or pay my card in full?

-

When will home equity loan rates come down?

-

2. Plan to tackle high-interest debt

-

Credit bureau self-service websites

-

How did the mifepristone case make it to the Supreme Court?

-

2024 SSI maximum benefit amounts

-

Ways to beef up your 650 credit score

-

What is required to be approved for a HELOC or home equity loan?

-

What can I add on to YouTube TV?

-

A mortgage diversifies your credit

-

How to put your house in a trust

-

YNAB, for hands-on zero-based budgeting

-

Who should get a cash-out refinance?

-

2. Get your finances in order

-

How do I know if I received an overpayment?

-

Balloon mortgage pros and cons

-

Do get a home inspection for new construction

-

Pros of getting a fixed-rate HELOC

-

Family trust vs. living trust

-

How much cash can you get from a cash-out refinance?

-

When will lenders use it?

-

2. Shopping for a house before a mortgage

-

What does Disney+ include?

-

How to freeze a child’s credit

-

How to maximize Social Security benefits for married couples

-

2. Reduce your internet speed for a lower price

-

How to make a home budget

-

Wedding planning is plagued by money struggles for many

-

How to calculate your credit utilization ratio

-

How to make a monthly budget

-

Filing Chapter 7 after a Chapter 7 discharge: 8 years

-

Advantages and disadvantages of reverse mortgages

-

How much should you tip an Uber driver?

-

The Fed is pushing to slow the economy

-

Best senior-specific plans

-

Revolving credit examples

-

2. Examine your situation

-

Home improvement project costs

-

What is an HOA and what does it do?

-

How do you set up a transfer on death (TOD) deed?

-

What assets count toward a high net worth?

-

Skip (for a couple of weeks): Toys and holiday decor

-

How does earnest money work?

-

What’s happening to Mint?

-

2. Use community marketplaces

-

Do Your Own Will benefits and drawbacks

-

Establish new study habits

-

SSDI benefits for bipolar

-

It’s usually best to delay

-

The timeline to lower inflation

-

What are long-term financial goals?

-

Risks can outweigh rewards

-

Understand that timeshares aren’t a financial investment

-

Tax benefits of owning a home

-

Is ‘pay for delete’ legal?

-

What to do about an old phone bill

-

Will I get stuck with family members’ debt after they die — or vice versa?

-

Work-from-home trend a factor, researchers say

-

Track your spending for a set period

-

Startups focus on paycheck-to-paycheck workers

-

2. Determine distribution

-

Lean on investments or savings, if you have them

-

What is the connection between debt and chronic pain?

-

2. You can earn and redeem rewards points

-

How does a nonworking spouse qualify for Social Security retirement benefits?

-

Buy: Father’s Day gifts

-

3. Do I qualify for any down payment assistance programs?

-

What to expect with a credit score simulator

-

How these new weight-loss drugs work

-

Where are layoffs happening?

-

How to approach the interview topics

-

Secured vs. unsecured debt

-

How do you file Chapter 7 bankruptcy?

-

Start with a spending plan

-

Which mortgages are assumable?

-

Late payments or bankruptcy

-

Why using a budget calendar matters

-

Pros and cons of a lady bird deed

-

Freezing your Experian credit report online

-

How does the Social Security Administration calculate a COLA?

-

How voluntary repossession affects your credit and finances

-

2. Become a virtual assistant

-

The mortgage underwriting process

-

Getting by on multiple income streams

-

What happens if I retire before age 65?

-

You might get a better mortgage rate by refinancing

-

2. Categorize your expenses

-

Uber vehicle requirements

-

How to write a late payment removal letter

-

Start your family budget with estimates

-

Why is beef so expensive?

-

When can a spouse claim Social Security spousal benefits?

-

How does a hard inquiry affect your credit score?

-

Who manages estate sales?

-

How to avoid repossession after missed car payments

-

What is a good FICO score?

-

Double-check advice and credentials

-

The rewards and challenges of being an entrepreneur

-

Is your advisor listening?

-

How to get SSDI benefits for fibromyalgia

-

Auto loans on your credit report

-

Waiting is best for most people

-

2. Enter your personal information

-

1. Make sure it’s legal

-

What are the Amazon Prime benefits?

-

How much to tip various service providers

-

Who qualifies for a loan modification?

-

What is included in an Equinox membership?

-

Be prepared to offer above the asking price

-

Know what happens when you can’t pay a bill

-

How do you report rental payments?

-

How credit scores affect auto loans

-

How do I access Prime Reading?

-

Why did GDP increase in Q2 2024?

-

3. Look for offers from cell phone carriers

-

Reduce the cost of activities

-

Use cash and credit cards in higher-risk situations

-

How can having a limited credit file affect you?

-

What’s at risk if you waive the home inspection?

-

Letters of administration vs. letters testamentary

-

Not all of the highest-paying jobs are on the list

-

How can I budget for my electric bill?

-

Note Poshmark’s seller fees

-

Leave 30% of your income for wants

-

2. Rakuten Cash Back Button

-

Plan for required minimum distributions

-

2. Get specific about your triggers

-

Debt is up, but delinquencies are down

-

Payment increases from continuing to work

-

What is the U.S. unemployment rate?

-

How much is Sling TV per month?

-

2. “Your benefits are suspended.”

-

How much does internet service cost per month?

-

How to read your escrow analysis

-

Costs — and acceptance — vary widely

-

What happened after the debt ceiling deal was reached?

-

How life expectancies can differ

-

How much does a Crunch Signature membership cost?

-

How to build credit from nothing

-

Refinance to a longer term

-

Tips to work on your 500 credit score

-

It’s not how many cards, but how you use them

-

Not getting good advice can be costly

-

Can I get a replacement Social Security card at my local office?

-

First-time home buyer grants in West Texas

-

Rules for refinancing conventional loans

-

2. Use the FHFA House Price Index Calculator

-

How much does it cost to make a will?

-

How conservatorship works

-

What identity theft protection services do

-

How to find bank-owned properties

-

How much does IDShield cost?

-

State minimum wages in 2024

-

Do be there for the home inspection

-

How to make money as a novice

-

Steps to getting a cash-out refinance

-

Where can I get FICO Score 9?

-

NCHFA first-time home buyer loan programs

-

If your credit score is 700 or above

-

Visit on a day with free or reduced admission

-

What to look for in a credit counseling agency

-

Who will the UltraFICO score help?

-

When does the home inspection happen?

-

How to close your bank account so your credit isn’t affected

-

SSDI benefits for long COVID

-

Can you freeze your Social Security number?

-

How do reverse mortgages work?

-

Our take on the end of credit card rewards

-

Georgia first-time home buyer programs

-

How closing a credit card can affect your score

-

CHFA highlights and eligibility requirements

-

2. Take note of 401(k) fees

-

3. Buy a pre-owned iPhone

-

2. Homeowners insurance claim

-

Homebuying budgets may need a reality check

-

Understand how subscriptions impact your finances

-

3. Look for last-minute deals

-

Examine recent spending, then ruthlessly reduce

-

Try to bring more money in

-

What is the purpose of a holographic will?

-

What is a reasonable wedding budget?

-

What to consider before joining a gym

-

Alternatives to Fabric by Gerber Life

-

How much of my private disability insurance income is taxable?

-

Savers could pay more for Medicare — and cost their kids

-

How much does AdSense pay?

-

Is Amazon Music free with Prime?

-

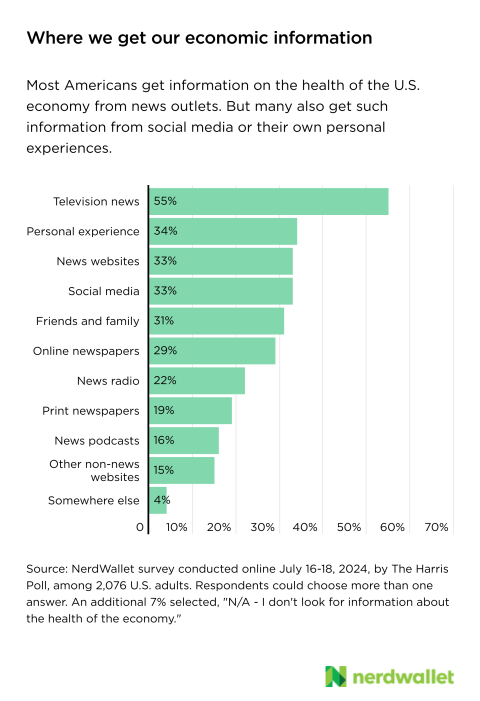

Reliable information is key — and readily available

-

How to avoid overpaying for cable

-

What day is my September 2024 payment coming?

-

$125 million on check-cashing services

-

Why does a high DTI affect new credit?

-

Supply chain issues could resurface

-

How to get a tax lien removed

-

But scores don’t tell the whole story

-

What to do if you’re having trouble making your payments

-

3. Choose a payoff method

-

How to write a thank-you email after an interview

-

2. Available homes may not be perfect homes

-

Types of special needs trusts

-

VantageScore 3.0 vs. VantageScore 4.0

-

New York state first-time home buyer programs

-

Zero-based budgeting example

-

Just starting out? Get on the credit radar

-

Recent weather events around the U.S.:

-

Who offers first-time home buyer education?

-

Why are eggs so expensive?

-

3. An Airbnb or hotel rental

-

Mortgage payoff calculator help

-

MSHDA first-time home buyer loan programs

-

What to do if you spot a problem

-

The measure of low income can vary

-

What is a home equity loan?

-

How do I pay back a Social Security overpayment?

-

Debt relief options to consider

-

Are paid surveys worth it?

-

Itemizing or taking the standard deduction

-

What information do you need to freeze your credit?

-

How to pay for a bankruptcy

-

How long do children receive Social Security benefits?

-

3. Ask for manufacturer coupons

-

What’s the difference between a HELOC and a cash-out refinance?

-

Cons of getting a fixed-rate HELOC

-

How to set up a family trust

-

How to build your credit score

-

Our take on student loan cancellation

-

3. Recover unclaimed money

-

MHDC highlights and eligibility requirements

-

What is a government shutdown?

-

WSHFC first-time home buyer loan programs

-

Learn what to expect before you shop

-

How to set up an irrevocable trust

-

Do you have to tip pizza delivery drivers?

-

Take a break from spending in the new year

-

Why your full retirement age matters

-

Filing Chapter 13 after a Chapter 13 discharge: 2 years

-

How does the VA calculate disability ratings?

-

4. Pay attention to prices

-

WHEDA first-time home buyer programs

-

2. Double-check your insurance

-

How many credit cards should I have?

-

First-time home buyer grants across Florida

-

How does having a high net worth impact your financial life?

-

What can I do if I make a late payment?

-

2. Your credit card balance is higher than usual

-

Buy: Small kitchen appliances

-

What is the average American net worth?

-

How does a housing co-op work?

-

Is 0% credit utilization bad?

-

Which states have Miller trusts?

-

4. Invest in a digital antenna

-

Do I need an estate planning attorney?

-

How a charitable remainder trust works

-

Key differences between caskets and coffins

-

What to know about Social Security disability benefits

-

What are the types of bankruptcy?

-

How landlords and property managers check credit

-

Can I get both SSDI and SSI?

-

Build if you want to call the shots

-

Trade the gift card for cash

-

Should you hire a real estate attorney?

-

How to dispute your Equifax report online

-

Where to find a lender that offers HELOCs for investment properties

-

Tactics to try at the box office

-

Don’t buy a timeshare on vacation

-

MFA highlights and eligibility requirements

-

How long do collection accounts stay on your credit reports?

-

Other options with no credit check

-

2. Research the domain history

-

Who offers first-time home buyer assistance?

-

Why you may want to refinance

-

PHFA first-time home buyer loan programs

-

How much does a will cost?

-

3. Think about your children

-

4. What is my interest rate?

-

How to set up a financial power of attorney

-

Reach out to local and national resources

-

2. Use part of your down payment to pay down debt

-

How much you can get from an immediate annuity

-

How to attract clients and succeed

-

How an adverse action notice can help you

-

How to determine the work needed and your budget

-

Why is budgeting important?

-

Make a digital assets inventory

-

Understand how much data your apps use

-

3. Transcribe audio and video

-

What data do the credit bureaus maintain?

-

How the Social Security first year of retirement rule works

-

Distinguish between good debt and bad debt

-

Yes, gas prices have gone up

-

How much rent can you afford?

-

Calculating net worth: What are assets and liabilities?

-

Home equity loan rates in 2024

-

Other alternatives to Mint

-

How much do virtual assistants make?

-

What it takes to get a good FICO score

-

3. Getting just one quote for mortgage rates

-

When will beef prices go down?

-

NerdWallet’s budget planner

-

What to look for in a personal finance tool

-

How to apply for Social Security

-

Is your advisor leaning in?

-

What are the pros and cons of using home equity to pay off debt?

-

Pros and cons of revocable living trusts

-

Look for lower interest rates and ways to pay more

-

Working from home job ideas

-

Our take on canceling luxury credit cards

-

How long do recessions last?

-

What are the credit score ranges?

-

3. Request a credit report or reports

-

How much of your wages can be garnished?

-

Outdoor furniture: Summer, fall

-

3. Don’t assume — ask

-

2. Determine how your buyer’s agent gets paid

-

How does mortgage forbearance work?

-

A long non-winning stretch, but still hope

-

Mortgage recast requirements

-

How the cash stuffing method works

-

How you can prepare for the end of Mint

-

3. Layer on coupon codes and cash back

-

3. Register for rewards programs and free trials

-

One for the money, two for the show

-

How do I borrow an item from Prime Reading?

-

What other ownership structures exist?

-

What do employers see in a hiring credit check?

-

How to get letters of administration

-

Tips for navigating a seller’s market

-

Retiring and Social Security can be separate decisions

-

What a mortgage payment includes

-

How to make more money on Poshmark

-

Create holiday spending categories

-

3. “You can pay to increase your benefits.”

-

Ways to lower your monthly mortgage payment

-

What are the three main types of appraisals?

-

Get creative to reduce expenses and increase income

-

What to include in your debt verification request

-

What can credit repair services do?

-

Information you’ll need

-

What is a credit limit and where can you find it?

-

Can you collect both spousal benefits and your own retirement benefit?

-

Let your goals inform your habits

-

Are Prime Day sales worth shopping?

-

Identify your next-level priorities

-

What to wear to a job fair

-

Is Chapter 7 bankruptcy right for you?

-

How to meet your monthly savings goal

-

TransUnion credit freeze by postal mail

-

Other first-time home buyer resources

-

How to create your monthly budget calendar

-

CalHFA first-time home buyer loan programs

-

When to use a credit freeze

-

13 fundamentals of personal finance

-

Responsibilities of an attorney-in-fact

-

Can you collect Social Security divorced spouse benefits and your own retirement benefits at the same time?

-

How to buy a bank-owned home

-

What to know about working in the gig economy

-

Does raising the minimum wage cause inflation?

-

A balloon mortgage could be hard to find

-

How to know who your mortgage servicer is

-

Step 3: Research the top places to make money online

-

Uber insurance requirements

-

What’s being done to bring about change

-

A trusted contact could thwart fraud

-

When will the government shut down?

-

Look for flexible pricing policies

-

Different levels of coverage

-

How much do estate sale companies charge?

-

Money talk is difficult for some, but a necessary premarital task

-

How can I re-apply for SSDI benefits through the five-year rule?

-

Use a credit utilization calculator

-

What experts say about Biden’s economic plans

-

How much do Uber drivers make per hour?

-

5. Buy the Sunday paper (for coupons)

-

What are the steps for getting a POA in Virginia?

-

How to plan your kitchen remodel

-

Alternatives to closing a credit card

-

Your car is a taxi cab and your primary tool

-

3. Decide if you’ll rent to friends or strangers

-

Is the CHOICERenovation loan right for you?

-

How do you make money on TikTok Shop?

-

Types of loan modification programs

-

Advantages of a transfer on death deed

-

Skip: Clothes you want to fit well and feel comfortable

-

Maximize your down payment

-

Consider language choices carefully

-

What to do if you can’t catch up on your bills

-

Alternatives to Do Your Own Will

-

Mausoleum costs vs. gravesite costs

-

Be wary of texts, calls or unsolicited requests

-

How to thicken your credit file

-

How much time does a home inspection actually take?

-

The inflation-matching savings account

-

What types of bipolar qualify for disability?

-

How mortgage forbearance works

-

Types of second mortgages

-

Commit 20% to savings and debt repayment

-

What services could shut down?

-

3. Use envy as a motivator, not a detractor

-

2. Try to keep most of your credit limit available

-

Should you tip all kinds of massage therapists?

-

Don’t wait too long to consider bankruptcy

-

How does Social Security work?

-

Debt-to-income ratio tops denial reasons

-

Can I be arrested for debt?

-

Who pays for escrow services?

-

How much will paying off my credit card benefit my score?

-

Apply for mortgage forbearance

-

Buyers would set their agents’ pay

-

But home prices won’t fall much, if at all

-

4. Open a high-yield savings account

-

Comparison shop in advance

-

Make more of what you spend

-

Why checking your credit is smart

-

How exactly does early retirement reduce my Social Security benefit?

-

Buying and budgets in 2024

-

Other tools to check your financial health

-

Types of financial power of attorney

-

Update your privacy settings

-

What is a home equity line of credit (HELOC)?

-

What day is my October 2024 payment coming?

-

Advantages of putting a house in trust

-

Rules for refinancing FHA loans

-

Strategies to build your 695 credit score

-

Should I choose a home equity loan or a HELOC?

-

What does a home warranty cover?

-

What midsize counties have the lowest climate change risks?

-

Are identity theft protection services worth it?

-

How much are children’s Social Security survivor benefits?

-

4. Search a coupon database or app

-

Don’t get in the home inspector’s way

-

What happens during a recession?

-

3. Build a budget that works for your expenses

-

Cash-out refinance requirements

-

Why financial goals matter

-

If your credit score is lower than 700

-

Does Disney+ allow password sharing?

-

Rental website data has shown rent growth slowing for some time

-

How is a FICO score calculated?

-

Do delivery fees go to drivers?

-

What’s going on with layoffs in tech?

-

Filing Chapter 7 after a Chapter 13 discharge: 6 years

-

Two kinds of reverse mortgages

-

Is IdentityForce worth the price?

-

Claim Social Security before or after retiring

-

4. Successfully answer security questions

-

3. Compare your 401(k) to an IRA

-

3. There’s a mistake in your credit report

-

How to calculate your net worth

-

International roaming: prepaid

-

The economy negatively impacting outlooks

-

5. Borrow with your library card

-

Quitclaim deed tax implications

-

4. Explore alternative accommodations

-

GoodTrust benefits and drawbacks

-

How to plan a wedding on a budget

-

How should I organize records?

-

How much more will you need to retire?

-

How does Apple Music fit into your budget?

-

Will your disability benefits change when you turn 65?

-

How to defuse the tax bomb

-

Manufactured vs. modular homes

-

Payment decreases from continuing to work

-

Increase in inventory is just a drop in the bucket

-

Why ‘pay for delete’ is becoming outdated

-

2. Don’t apply for credit too often

-

How ADUs are like swimming pools

-

3. Test out customer support

-

3. Buying in 2022 will still be tough

-

How debt affects finances when you have chronic pain

-

How the second SSI payment will be paid

-

Shop now: Semiannual sales

-

3. Use home buyer assistance programs

-

Leaning on others takes the pressure off of just you

-

Help with specific purchases

-

How much is YouTube TV for 1 year?

-

How do you start a budget?

-

Median down payment by age

-

How much can the windfall elimination provision reduce my Social Security benefits?

-

3. Get a comparative market analysis

-

8 common mistakes in DIY wills

-

How to avoid voluntary repossession

-

3. Make a plan for the down payment

-

Programs that use the federal poverty level

-

7 types of identity theft and the warning signs

-

Give yourself a retirement raise

-

How much more will I get if I put off retirement?

-

Buying a manufactured home

-

How to place a fraud alert

-

How to get a fixed-rate HELOC

-

How much is YouTube Music?

-

Check your debt-to-income ratio

-

4. Get down payment assistance for a home

-

Who is affected by a government shutdown?

-

What do deposit accounts have to do with credit?

-

Seek out new perspectives

-

2. Build a money management blueprint

-

Revocable living trust vs. will

-

Pros and cons of revolving credit

-

Home improvement project rate

-

Updates to the FDCPA rules

-

General furniture-buying tips

-

4. Treat Europe like a theme park

-

Impose a 10% import tariff

-

Is earnest money refundable?

-

What makes an energy-efficient home different?

-

How to set up a Miller trust

-

Can ‘Barbie’ success be replicated?

-

Enlist a teaching assistant

-

Who is tenancy in severalty right for?

-

Does an employer credit check hurt your score?

-

6. Bundle cable and internet

-

SSI vs. SSDI: Key differences

-

Where is a holographic will valid?

-

In-demand jobs that pay the most money

-

How to lower your electric bill

-

How to dispute your Equifax report by mail

-

Pros and cons of buying a townhouse

-

What programs would continue?

-

Consider account conversions

-

What’s included in a Gold’s Gym membership?

-

Reason No. 2: Rising interest rates

-

Create a money-making strategy

-

Amazon Music Prime vs. other streaming services

-

2. Pay it off in one lump sum

-

How fast are wages growing?

-

What day is my October 2024 payment coming?

-

Avoid risky concentrations

-

Ignoring financial stress is ‘like bailing a leaky boat’

-

How financial planners estimate life expectancy

-

First-time home buyer benefits and programs

-

Examples of thank-you emails

-

Space out credit applications to minimize impact

-

Choose the least expensive high-interest debt

-

Credit-building strategies

-

When you need to contact all bureaus vs. just one

-

Can a nonworking spouse get benefits if their working spouse hasn’t yet filed for Social Security?

-

Fewer cravings could be a blow to Big Snacks

-

What’s at stake in the SCOTUS mifepristone case?

-

2. If a collection is on your report in error, dispute it

-

Get a secured credit card

-

What is covered in a first-time home buyer class?

-

Mortgage payments vs. rent

-

How does a COLA apply to Social Security payments?

-

3. Comparison shop between brands (the discount ones aren’t always cheapest)

-

How to pay off a mortgage early

-

When should I close my credit card?

-

What happens when you get your car repossessed?

-

What if I think the Social Security Administration is wrong?

-

Do all workers earn at least the minimum wage?

-

5. Visit retailer websites and apps

-

How to become a virtual assistant

-

Who can get a death certificate?

-

Why do lenders sell mortgage loans?

-

How to calculate debt-to-income ratio for a mortgage

-

How to apply for Social Security spousal benefits

-

Do you have to tip in cash?

-

Reasons to buy a house with cash

-

What is a VA combined disability rating?

-

What happens if you don’t tip?

-

Objecting because of financial hardship

-

6. Avoid online grocery shopping

-

Where can I get a power of attorney form?

-

What to know about car loan shopping

-

FAQ about freezing and unfreezing credit

-

Potential issues with having multiple credit cards

-

What you can do about wage garnishment

-

Cons of a condo vs. a house

-

4. Learn your store’s coupon policy

-

There could be bumps in the road ahead

-

What causes a bad credit score?

-

What is a FICO Auto Score?

-

4. Get to know your local stores

-

Does Hulu allow password sharing?

-

Is Amazon Prime Reading the same as Kindle Unlimited?

-

Lottery payout options: Annuity or cash?

-

How did personal income change in Q2 2024?

-

When is an appliance or system covered?

-

Give yourself the chance to make a choice

-

Can you change the trustee after selecting one?

-

State taxes on disability income

-

3. Get a secured credit card

-

3. Build an emergency fund

-

Is the debt avalanche method for you?

-

How to improve your credit mix

-

4. “You owe money that has to be paid immediately.”

-

Budgeting for both needs and wants

-

Potentially overlooked (or underestimated) ways to save

-

Negotiations would be more complex

-

Is there a diesel shortage?

-

Beware the Social Security tax torpedo

-

Documents you’ll need to replace a Social Security card

-

Frugal entertainment tips

-

How can Latino individuals and families help build trust in financial systems within their communities?

-

2. Apply for a medical credit card

-

TransUnion credit freeze by phone

-

Keep your inventory safe — and updated

-

Rules for refinancing VA loans

-

Where do the credit reporting bureaus get their data?

-

Don’t worry about the rest

-

Average gas price per state

-

Do you include a 401(k) in a net worth calculation?

-

Ways to get the best home equity loan rates

-

Collect the right tax forms from your lender

-

How long does a credit freeze last?

-

How Paramount+ fits into your budget

-

Don’t be afraid to negotiate with the seller

-

How to stop spending money on food

-

Goodwill letter vs. credit dispute letter

-

Then get a baseline of your expenses

-

Our take on personal finance

-

Missouri home buyer assistance programs

-

How to pay off debt and help your credit score

-

3. Negotiate with your internet provider for a better deal

-

The Federal Trade Commission’s budget worksheet

-

Use military, senior or other discounts

-

What you’ll need to apply for Social Security

-

Don’t feel pressure to buy gifts

-

Does Experian Boost actually build your score?

-

Waiting until after full retirement age to claim benefits

-

Does age affect your credit score?

-

How to budget and make trade-offs

-

Filing Chapter 13 after a Chapter 7 discharge: 4 years

-

How much will you need to retire?

-

5. Generate your credit report online

-

How to start a TikTok Shop as a seller

-

Disadvantages of transfer on death deeds

-

How do you become a HNWI?

-

How are state labor markets doing?

-

How to update your Social Security card

-

What happens when mortgage forbearance ends?

-

Why is net worth important?

-

How credit utilization affects your scores

-

What to look for in a new budgeting app

-

5. Ask insurance and health care providers

-

Make the friendship bracelets … and buy a shirt

-

4. Home improvement loans

-

Quitclaim deed vs. warranty deed

-

5. Pick a different neighborhood

-

Set yourself up for next summer

-

Other perks that come with a membership

-

How likely is it that the SSA will approve my SSDI application?

-

TDIU qualification examples

-

What else could be disrupted?

-

Pros and cons of choosing a HELOC

-

4. Recognize what you don’t see

-

Is Honey available as an iOS or Android app?

-

How to write a ‘pay for delete’ letter

-

Pros, cons and differences

-

Is there a maximum amount of debt I can take on?

-

Who to contact for more information

-

$46 million on nonbank money orders

-

What could have happened if the U.S. defaulted?

-

What is an escrow account?

-

What should I do if my DTI is too high?

-

Keep an eye on your progress

-

Apply for loan modification

-

1. Derogatory mark: Missed payments

-

5. Use your credit card benefits

-

How much does credit repair cost?

-

How to start a zero-based budget

-

Can you qualify if you’re divorced?

-

How to prevent someone from contesting a will

-

5. What is the annual percentage rate?

-

Layoffs spiked among tech companies in 2023

-

4. Ask the seller to finance the purchase

-

Why is there an egg shortage?

-

Advantages of assumable loans for sellers

-

Your U.S. credit score won’t follow you

-

What you can learn from your budget calendar

-

Disadvantages of putting a house in trust

-

2. Consider debt consolidation

-

Adjust phone and app settings to save data

-

What to do after a repossession

-

What most populated counties have the lowest climate change risks?

-

What to know if you take online surveys

-

You could save by changing your home loan’s term

-

How do streaming services fit into your budget?

-

Pros and cons of family trusts

-

3. Keep managing your investments

-

How much do Uber drivers make?

-

4. Not checking credit reports and correcting errors

-

Wipe out toxic debt first

-

Can Disney+ fit my budget?

-

Beware fraudulent email requests

-

How are estate sale items priced?

-

Be firm on your needs, flexible on the rest

-

What to complete before re-filing for SSDI benefits

-

Is per-card or overall utilization more important?

-

How to get medical bills off credit reports

-

Getting ready for a recession

-

New CHOICERenovation provisions

-

Cons of reverse mortgages

-

Potential employers may ask about it

-

Buy: Batteries, cables and phone cases

-

Be straightforward about financial hardships

-

Game apps that pay real money: before you play

-

4. You’re a victim of identity theft

-

Benefits of recasting a mortgage

-

How does Hulu fit into your budget?

-

6. Share a friend’s or relative’s account

-

Can a retired person file for disability benefits?

-

7. Negotiate a lower rate

-

The state of home improvements

-

4. Get a credit-builder loan or secured loan

-

How is a modular home built?

-

Borrow for the right reasons

-

3. Raise your credit limit

-

4. Triple-check the return policy

-

Sales will happen early and often

-

4. Find a budget that works for you

-

Pros and cons of refinancing a home equity loan

-

Dispute hard inquiries that don’t belong to you

-

4. Current home prices could bust budgets

-

Who uses VantageScore 4.0?

-

Exceptions to the windfall elimination provision

-

How to check your credit score without hurting it

-

What factors determine your credit limit?

-

Wait for: Amazon Prime Day

-

How to find your child’s Social Security number

-

How to budget for variable and fixed expenses

-

Pay attention to insurer ratings

-

3. Consider other credit options

-

How cash-out refinances and HELOCs are similar

-

Address reasons cited in adverse action letter

-

Lifting a TransUnion credit freeze

-

Does YouTube TV allow password sharing?

-

Try a simple budgeting plan

-

Who does the windfall elimination provision affect?

-

Freezing your Experian credit report via postal mail

-

Rules for refinancing USDA loans

-

4. Hire a professional appraiser

-

Alternatives to a cash-out refinance

-

When voluntary repossession makes sense

-

Are the paid My Best Buy memberships worth it?

-

2. Gather materials to dispute errors

-

How to remove or replace an attorney-in-fact

-

How do you freeze your child’s credit?

-

How to apply for children’s Social Security survivor benefits

-

6. Check the Sunday newspaper

-

Can I lift a fraud alert?

-

What’s involved in the probate process?

-

Consider a home equity loan

-

Strategies to keep building your 720 credit score

-

Average monthly expenses that increased year over year

-

Am I eligible for a reverse mortgage?

-

How to get a VantageScore

-

7. Calculate your burn rate

-

How does revolving credit impact your credit score?

-

How much does it cost to get a power of attorney in Virginia?

-

What to do if you aren’t eligible or aren’t approved for HAF

-

5. Prioritize flexibility

-

CHFA first-time home buyer loan programs

-

How to get a mortgage loan modification

-

How long does a late payment stay on my credit report?

-

Leverage your earning power

-

Getting a loan for a co-op

-

Other factors can help you buy a car with bad credit

-

5. Talk to friends and family about scaling back

-

How did GDP in 2023 compare to recent years?

-

How to choose the right budget system

-

How to decide whether you should be a trustee

-

What are your legal rights?

-

Inflation is not the same for everyone

-

A few tips about giving gift cards

-

Qualifying for a second mortgage

-

How much will a real estate attorney cost?

-

Make charitable contributions

-

How do you install the Honey extension for Chrome?

-

Buy in attractive locations

-

4. Brainstorm ways to increase income, if needed

-

How much does Social Security pay?

-

Getting an approval: Improving your odds

-

Overspending is common, despite monthly budgeting

-

Older adults are the biggest target

-

When and how to talk about money

-

How much does a Crunch+ membership cost?

-

6. Make your will official

-

3. Rewards can offset the membership fee

-

How is my Social Security benefit determined?

-

Move up the care ladder slowly

-

What comes with a 24 Hour Fitness membership?

-

Now consider everything else

-

Rebuilding after bankruptcy

-

TaskRabbit jobs to consider

-

Prepare for additional supervision and appraisals

-

Know when the HELOC draw period ends

-

Goodbudget, for hands-on envelope budgeting

-

When does it make sense to hire a lawyer to make your will?

-

How to get a home equity loan

-

When to use a credit lock

-

Compare identity theft protection services

-

Can your ex’s current spouse collect spousal benefits if you do?

-

Choosing a manufactured home lot

-

How to make money as a Twitch Affiliate

-

Why death certificates can be helpful

-

Is YouTube Premium worth it?

-

Other notable required minimum distribution (RMD) rules

-

Understanding the appraisal process

-

Tips for avoiding late payments

-

5. Find tax credits for health insurance

-

How to calculate Social Security spousal benefits

-

Hard credit inquiry or soft inquiry?

-

When was the last government shutdown?

-

Some engaged Americans are having regular money fights

-

Does the cost of FuboTV fit into your budget?

-

What are the alternatives to foreclosure?

-

Is the debt snowball method for you?

-

Consider a “slush fund” for car costs

-

What you can do about money shame

-

Does Max cost the same as HBO Max did?

-

Programs in the Florida Panhandle

-

What to do when you get a garnishment judgment

-

Alternatives to a transfer on death (TOD) deed

-

How to improve bad credit

-

How to find an energy-efficient home

-

Types of power of attorney

-

Prime Reading vs. Kindle Unlimited

-

Upgrade your cyber hygiene

-

Do you have to contact anyone to switch from SSDI to Social Security?

-

How much does a Gold’s Gym day pass cost?

-

Reason No. 3: Bigger jackpots mean more tickets sold

-

Relish the challenge of being frugal

-

MFA first-time home buyer programs

-

Qualifying for a HELOC in retirement

-

Social Security disability benefits pay chart for 2024

-

4. Make rent and utility payments count

-

Will bankruptcy erase all my debt?

-

Compensation that fits your case

-

Ways to cope with debt when you have chronic pain

-

Can you receive benefits if your working spouse dies?

-

Bonus: Quirky observances

-

Have a thin credit file? Become scorable

-

Documents needed if you’re changing or correcting your Social Security card

-

But these slimming drugs come at a hefty price

-

Social interaction is good for development and business

-

What would Harris or Trump do for the economy?

-

Advantages of assumable loans for buyers

-

Tackle debt to save on interest

-

Grant programs in North Texas

-

Average down payment by state

-

Things to remember about working while on Social Security

-

How do you set up a lady bird deed?

-

Use Wi-Fi (instead of cellular) to save data

-

Rules for refinancing jumbo loans

-

4. Target (with Target Circle)

-

Full retirement age – Social Security

-

How to appeal a Social Security overpayment

-

How do you find out how much equity is in your home?

-

How much retirement income will you have?

-

How does a home equity loan work?

-

What else affects my Social Security benefit amount?

-

How to contact your servicer

-

How to maximize earnings as an Uber driver

-

Find out how much home equity you have

-

Weigh your in-store options

-

Does leasing a car build credit?

-

Net income for independent contractors

-

What to do once your Equifax credit freeze is in place

-

Top rental increases and decreases in the U.S.

-

4. Bundle your services for a better combined price

-

What questions should you ask an estate sale company?

-

What is a FICO score used for?

-

How much does a home inspection cost?

-

Boost vs. UltraFICO and eCredable Lift

-

What happened at the first presidential debate?

-

Should you get a home equity loan or HELOC?

-

What if my previous case wasn’t discharged?

-

How much should you spend on a mattress?

-

How high is your net worth?

-

How to cancel an Equinox membership

-

How long does mortgage forbearance last?

-

5. Someone else used your credit card account

-

How to increase your net worth

-

5. Make a shopping list and use apps for more savings

-

When can the seller keep my earnest money?

-

The pros and cons of paying yourself first

-

6. Reach out to religious groups and nonprofits

-

How to choose a casket or coffin

-

What a good credit score can get you

-

How to make a strong offer without waiving the inspection

-

Alternatives to GoodTrust

-

Some of the highest-paying jobs ‘don’t exist yet’

-

How to dispute your Equifax report by phone

-

What if you’re unhappy with your massage?

-

Store copies in the cloud

-

What internet speed do you need?

-

Connect with your community

-

$59 million on prepaid debit card fees

-

How do you solve a problem like the debt ceiling?

-

What is an irrevocable trust?

-

5. Pay with a credit card

-

How to qualify for first-time home buyer benefits

-

Plan when to claim Social Security

-

How to maintain your credit score

-

Eliminate mortgage insurance

-

What it means for buyers and sellers this spring

-

More new construction of single-family homes

-

How to boost your score after a hard inquiry

-

5. Borrowing for a home isn’t a sure thing

-

How can I repair credit myself?

-

Delaying Social Security benefits could trim your taxes

-

Current reads on the housing market

-

How can you get the best deals?

-

Get more help with monthly budget planning

-

Help them build their own wealth

-

Does YouTube TV offer offline viewing?

-

Will there be extra Social Security payments?

-

Other low-income guidelines and programs to note

-

How are gas prices determined?

-

No matter where you live, climate change will cost you

-

How to file for Social Security divorced spouse benefits

-

Pros and cons of HomeStyle renovation loans

-

Don’t assume the home inspector can be held liable

-

How long do recessions last?

-

5. Not having enough saved for a down payment

-

6. Apply for college grants

-

What to do after you find a budgeting template

-

Other tech tools to help you manage your money

-

Shop: Martin Luther King Jr. Day sales

-

What else you need to know

-

How to apply for VA disability benefits

-

8. Follow your favorite brands

-

What factors impact your credit scores?

-

Where to find a bridge loan lender

-

How to use the CHOICERenovation loan

-

4. Decide how much earnest money to offer

-

4. Assess income strategies

-

Invite kids to contribute

-

Will making a partial payment keep me from being reported late?

-

Skip (maybe): Tools and home improvement items

-

What happens if I cancel my Prime Membership?

-

7. Check your app store for free downloads

-

Who can help a trustee with their duties?

-

What to do if you notice signs your boss wants you to leave

-

It doesn’t squeeze your budget

-

Rebuilding your finances after bankruptcy

-

When can I start receiving disability benefits?

-

Freddie Mac and Fannie Mae mortgage assistance

-

What does this mean for your financial decisions?

-