Optical networking company Ciena (NYSE: CIEN) may not be a household name in the technology sector, but the stock has been in red-hot form on the market over the past three months, clocking impressive gains of 35% as of this writing.

However, a closer look at the company’s recent financial performance makes this recent rally seem surprising. Ciena’s revenue and earnings fell in the third quarter of fiscal 2024 (for the three months ended July 27). But investors seem to be upbeat about the potential turnaround in Ciena’s fortunes thanks to a rebound in telecommunications spending, as well as the growing adoption of artificial intelligence (AI).

Here’s a closer look at the reasons why Ciena could become a beneficiary of the proliferation of AI and sustain its newly found stock market momentum.

The worst seems to be over for Ciena

Ciena’s revenue in fiscal Q3 fell 12% year over year to $942 million, while non-GAAP (adjusted) net income dropped 41% from the prior-year period to $0.35 per share. These sharp declines were on account of the poor performance of the company’s networking business. More specifically, Ciena’s optical networking revenue fell 15% from the same period last year, while routing and switching revenue was down by 27%.

Ciena has been hit hard by the downturn in the telecom equipment market that began in the second half of 2023. According to market research firm Dell’Oro Group, global telecom spending fell by 17% in the first half of 2024. The decline in spending negatively impacted Ciena’s order book and the excess inventory that the company was left with has been weighing on its margins.

Dell’Oro estimates that telecom spending in 2024 could decline between 8% to 10%, up from the 4% drop seen last year. However, Citigroup points out that the scenario is improving in the North American telecommunications space, with spending expected to increase by 3% in 2025, compared to an identical decline estimated for 2024.

The good part is that Ciena is already witnessing an improvement in business conditions. The company reported a healthy order inflow in fiscal Q3, ending the quarter with a book-to-bill ratio of more than 1, which means that it received more orders than it shipped during the quarter. A reading of more than 1 is an indicator of strong demand for the company’s offerings.

Even better, Ciena’s inventory came down to $937 million last quarter from $1.2 billion in the same quarter last year. These positive developments indicate why Ciena’s outlook for the current quarter points toward an improvement in the company’s top- and bottom-line performance. The company is forecasting revenue of $1.1 billion in the current quarter at the midpoint, along with an adjusted gross margin of low to mid-40%.

The top-line guidance points toward a flat year-over-year performance, which would be a big improvement over the double-digit decline it reported in the previous quarter. Additionally, the gross margin forecast suggests that the bottom-line erosion is likely to slow down, as Ciena reported an adjusted gross margin of 43.7% in the fourth quarter of fiscal 2023.

Meanwhile, Ciena management and certain Wall Street analysts believe that the rapid adoption of AI is likely to give its addressable market and growth a nice boost in the future.

The need for faster connectivity in AI data centers should be a tailwind for Ciena

Morgan Stanley and Jefferies recently increased their price targets on Ciena stock citing the potential impact of AI on its business. While Morgan Stanley hiked its price target to $63 from $60, Jefferies has become more bullish on the stock with a price target of $80, compared to $65 earlier.

Jefferies points out that the potential jump in demand for faster connectivity between data centers to support the growth in AI workloads presents a solid growth opportunity for Ciena. Morgan Stanley has a similar stance, believing Ciena could clock a faster growth rate in the future thanks to the growing demand for data center interconnect (DCI) technology.

The investment banks have become more bullish about Ciena’s AI-related prospects following a recent presentation from the company in which it pointed out that global data center bandwidth is set to jump more than fourfold between 2023 and 2027. As a result, Ciena management believes that the demand for optical bandwidth could increase at a higher pace than the historical annual average of 25% to 30%.

The good part is that Ciena is already witnessing a positive impact on its business thanks to AI adoption. As management pointed out on the latest earnings conference call, “In Q3, we secured new wins with major cloud provider customers, spanning terrestrial, submarine and coherent pluggable applications, the majority driven by preparations for the expected growth in AI and cloud traffic.”

Dell’Oro Group estimates that the spending on back-end networks for connecting data centers to each other could double in the next five years, hitting $80 billion in annual revenue. So, don’t be surprised to see an acceleration in Ciena’s growth in the future; this is exactly what analysts are expecting from the company.

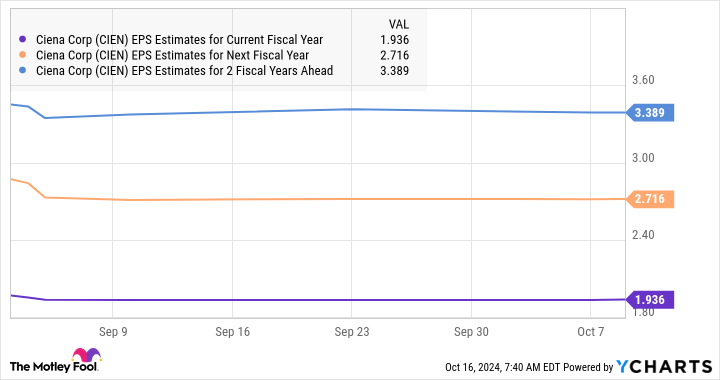

Ciena’s bottom line stood at $2.72 per share in fiscal 2023. That figure is set to drop this year, as the chart above shows. However, the company’s earnings are set to increase at an impressive pace over the next couple of years.

Assuming Ciena does hit $3.39 per share in earnings in fiscal 2026 and trades at 25 times earnings at that time (in line with its forward price-to-earnings ratio), its stock price could hit $85 in a couple of years. That would be a 25% jump from current levels. But if the market decides to reward it with a higher earnings multiple and the company manages to clock stronger earnings growth thanks to its improving addressable market, don’t be surprised to see Ciena delivering stronger gains.

Investors looking to buy a potential AI winner can consider buying Ciena, which is trading at an attractive 2.5 times sales and 25 times forward earnings, and whose bull run seems poised to continue.

Should you invest $1,000 in Ciena right now?

Before you buy stock in Ciena, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Ciena wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $845,679!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of October 14, 2024

Citigroup is an advertising partner of The Ascent, a Motley Fool company. Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Jefferies Financial Group. The Motley Fool has a disclosure policy.

Up 35% in 3 Months, This Tech Stock Could Become the Next Big Artificial Intelligence (AI) Play was originally published by The Motley Fool